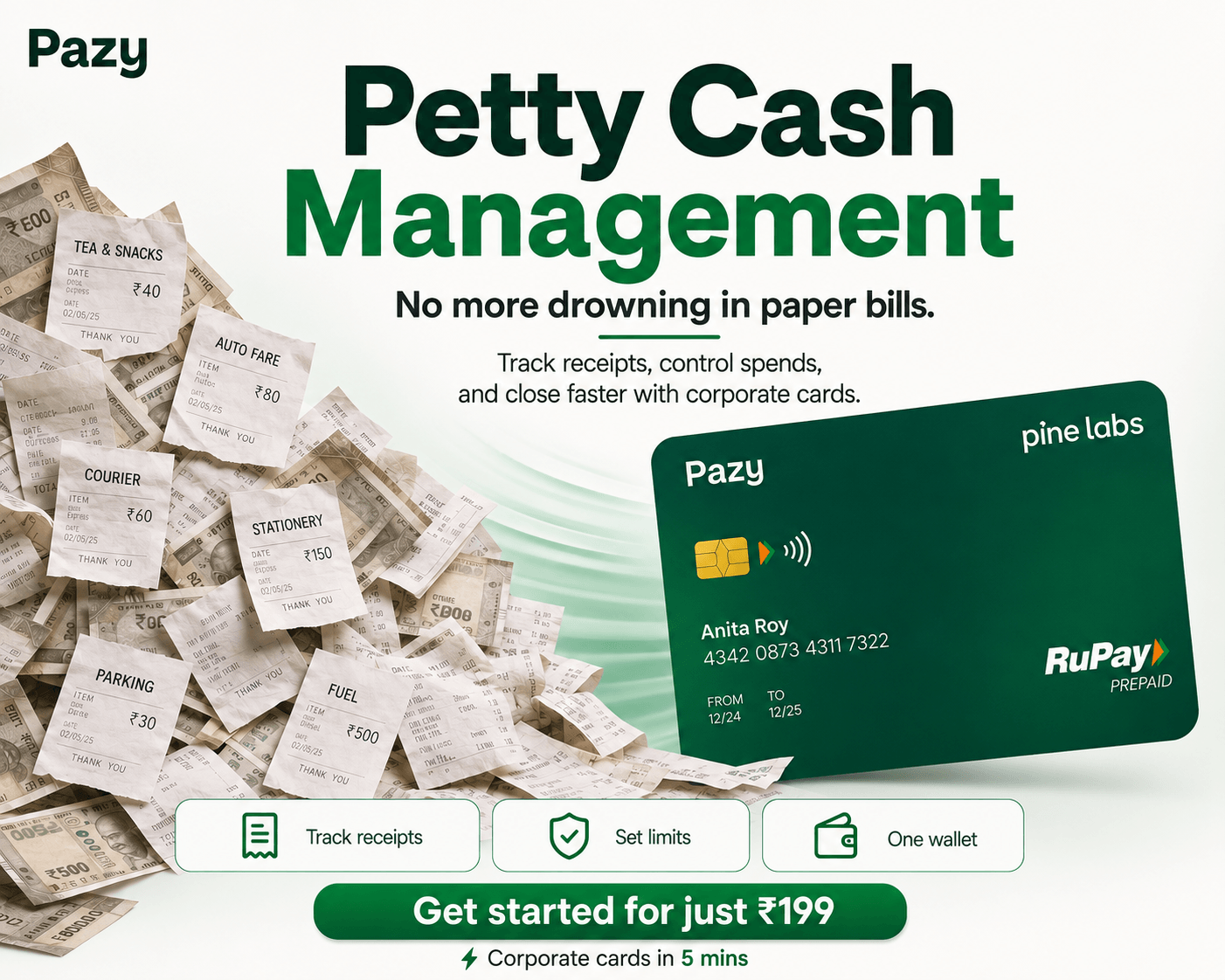

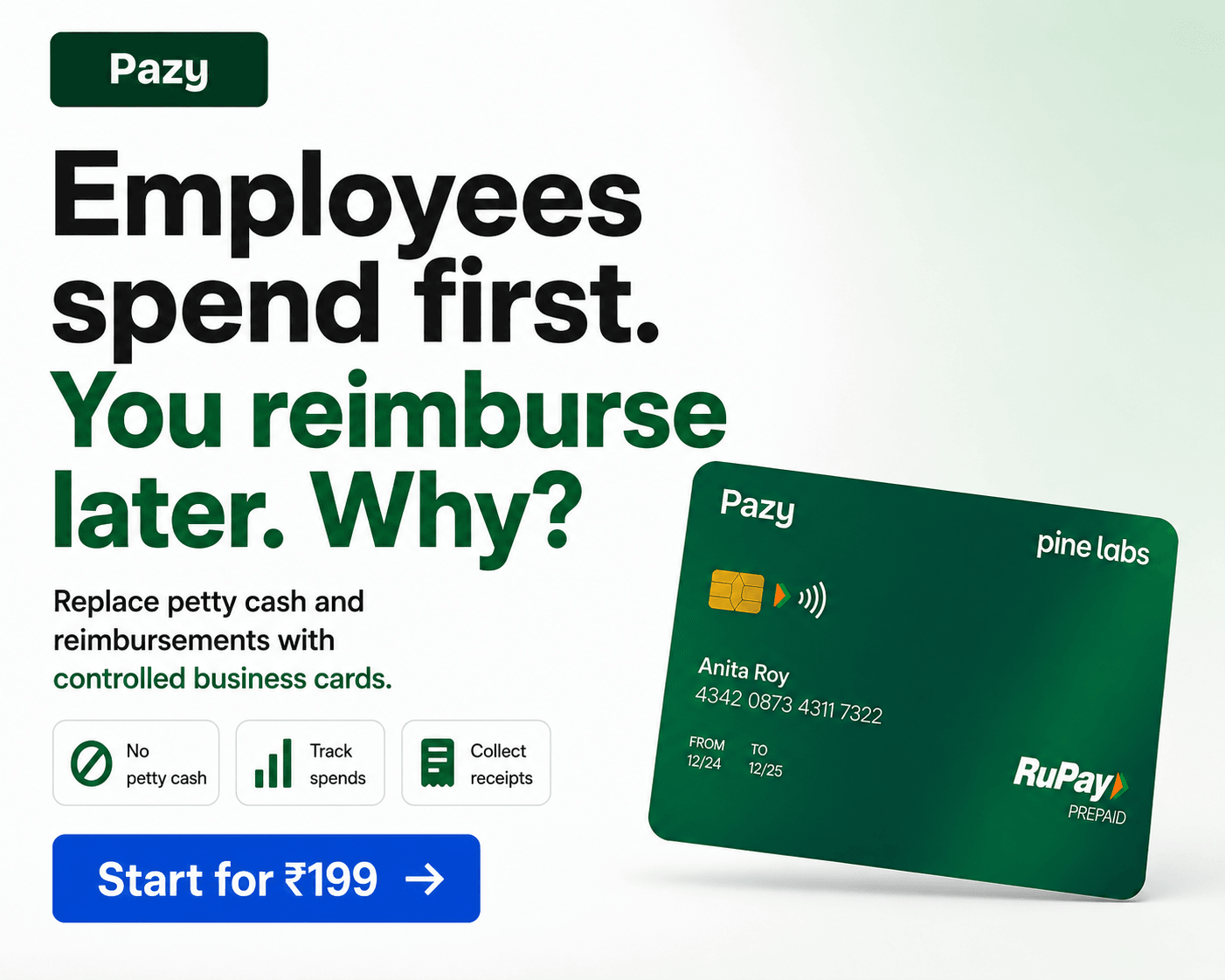

SaaS

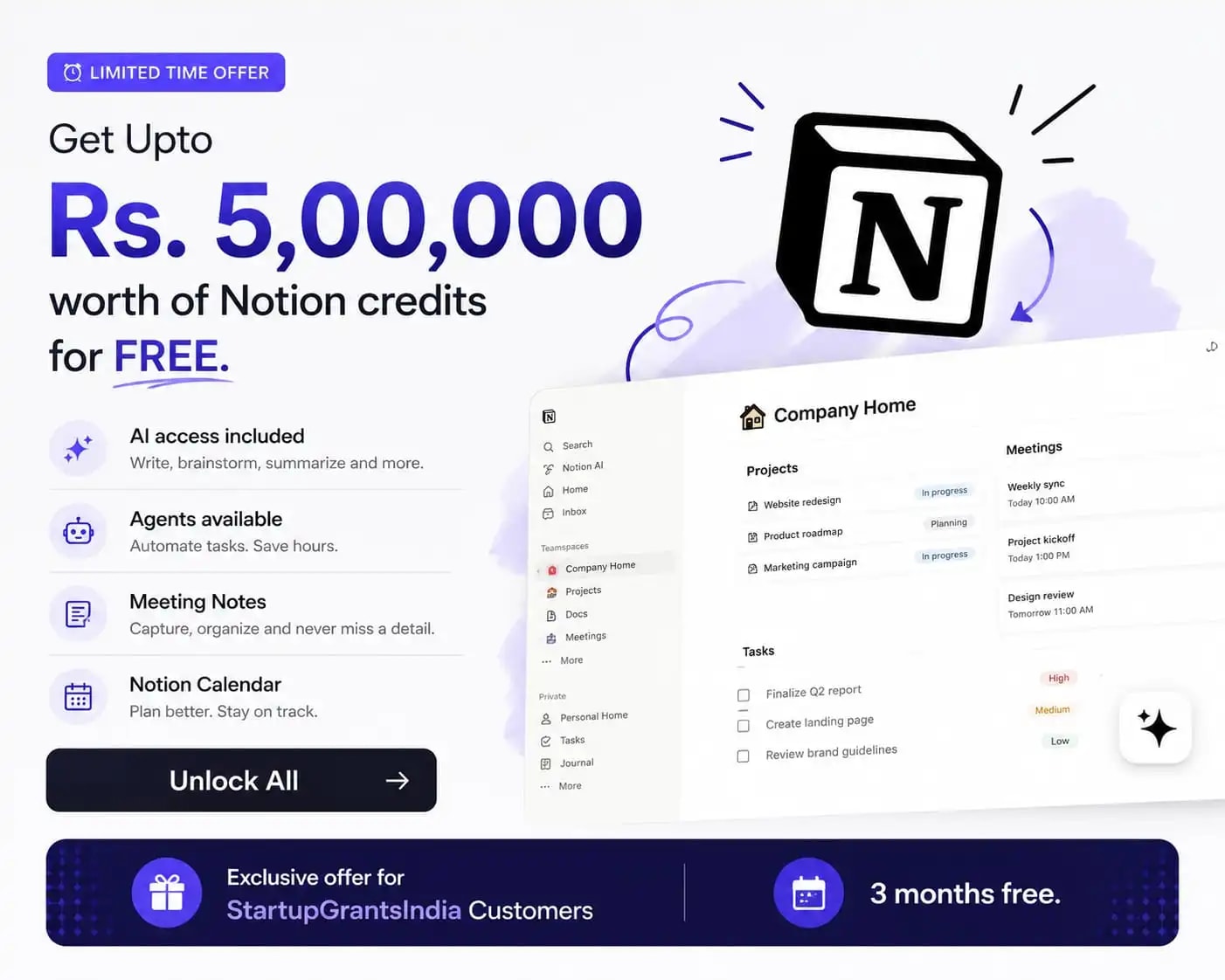

Rs. 5 Lakhs+ in Notion workspace credits — databases, wikis, project management, and team docs — for new users with a work email.

देखें कि क्या आपका फंडिंग राउंड धारा 56(2)(viib) एंजेल टैक्स को आकर्षित करता है — जारी मूल्य और FMV के बीच का प्रीमियम, अनुमानित कर, और क्या DPIIT पंजीकरण आपको छूट देता है।

Total amount the investor is putting in.

₹50 lakhs

The price per share at which shares are being issued to the investor.

₹150

FMV determined by a merchant banker or DCF method. DPIIT startups can issue at FMV without triggering tax.

₹100

DPIIT-recognised startups are exempt from angel tax under Section 56(2)(viib).

DPIIT-recognised startups are fully exempt from Section 56(2)(viib) angel tax.

This premium would normally be taxable, but DPIIT registration exempts it.

केवल अनुमान — यह वित्तीय, कर या कानूनी सलाह नहीं है। आंकड़े राज्य, पूंजी और व्यक्तिगत परिस्थितियों के अनुसार बदलते हैं।

यह जांचने के लिए चार संख्याएं दर्ज करें कि क्या आपका फंडिंग राउंड एंजेल टैक्स को आकर्षित करता है — और क्या DPIIT पंजीकरण आपको बचाता है।

एंजेल टैक्स, आयकर अधिनियम की धारा 56(2)(viib) का बोलचाल का नाम है। यह तब लागू होता है जब कोई असूचीबद्ध कंपनी — आमतौर पर एक स्टार्टअप — किसी निवेशक को उसके उचित बाजार मूल्य (FMV) से अधिक कीमत पर शेयर जारी करती है। इस अंतर को, जिसे शेयर प्रीमियम कहा जाता है, 'अन्य स्रोतों से आय' माना जाता है और लागू कॉर्पोरेट दर पर कर लगाया जाता है।

यह कर कंपनी द्वारा चुकाया जाता है, निवेशक द्वारा नहीं। स्टार्टअप निवेश के प्रीमियम हिस्से पर आयकर का भुगतान करता है।

DPIIT-मान्यता प्राप्त स्टार्टअप एंजेल टैक्स से पूरी तरह छूट प्राप्त हैं, बशर्ते उन्होंने DPIIT के साथ आवश्यक घोषणा दाखिल की हो। यह छूट विशेष रूप से एंजेल निवेश को वास्तविक स्टार्टअप में हतोत्साहित होने से रोकने के लिए पेश की गई थी। एक DPIIT स्टार्टअप किसी भी निवेशक को किसी भी प्रीमियम पर शेयर जारी कर सकता है, बिना धारा 56(2)(viib) को आकर्षित किए।

गैर-DPIIT स्टार्टअप अभी भी उत्तरदायी हैं। FMV आमतौर पर एक श्रेणी I मर्चेंट बैंकर द्वारा DCF (डिस्काउंटेड कैश फ्लो) विधि का उपयोग करके निर्धारित किया जाता है। उस FMV से अधिक कोई भी प्रीमियम कर योग्य है।

आयकर नियम असूचीबद्ध शेयरों के FMV को निर्धारित करने के लिए दो तरीके निर्धारित करते हैं:

DPIIT-मान्यता प्राप्त स्टार्टअप के लिए, छूट किसी भी विधि का उपयोग करने पर लागू होती है। अन्य के लिए, श्रेणी I मर्चेंट बैंकर से उचित DCF मूल्यांकन प्राप्त करना एंजेल टैक्स जोखिम को कम करने के लिए महत्वपूर्ण है।

कर प्रीमियम राशि का 30% है (साथ ही लागू अधिभार और उपकर)। यहाँ एक उदाहरण है:

एक गैर-DPIIT स्टार्टअप ₹150/शेयर पर ₹5 करोड़ जुटाता है। प्रति शेयर FMV ₹100 है:

कुल प्रीमियम = ₹50 × 33,333 = ₹16,66,667। 30% पर कर = ~₹5,00,000 प्लस अधिभार और उपकर।

Rs. 5 Lakhs+ in Notion workspace credits — databases, wikis, project management, and team docs — for new users with a work email.

7-day free trial of Semrush Pro or Guru — full SEO, keyword research, competitive audit, and rank tracking across India and global SERPs.

10% off Reclaim.ai Starter and Business plans for 12 months — AI scheduling assistant that auto-blocks focus time and defends your calendar.

Up to ~₹95L in Datadog credits covering the full observability stack — APM, logs, security, AI — for Series A or earlier startups.